How Can I Use Online Title and Escrow Services to Buy a Home in Albany, NY?

Summary

- Decide if your lender and attorney support remote notarization and e‑closing steps.

- Plan for wire safety and identity verification before sending any funds.

- Balance convenience against cases where in‑person work speeds up problem solving.

- Use Albany‑specific rules on title, taxes, and recording to avoid delays.

Introduction

Digital title and escrow tools can make an Albany, NY purchase more efficient, especially if you’re juggling work, travel, or a move into the Capital Region. These tools cover ordering title searches, opening escrow, wiring deposits, remote notarization, and e‑recording, all aligned to New York’s legal framework.

We’ve seen these systems reduce courier costs, cut days off turnarounds, and help out-of-area buyers close with less disruption. They are not a cure‑all. Albany County recording rules, lender requirements, and attorney practices still shape how “online” your closing can be. The most reliable outcomes come from aligning digital workflows with local norms.

What are online title and escrow services and how do they work?

Online title and escrow services digitize the steps that used to require in‑person visits, paper checks, and wet signatures. In practice, they include:

- Title search and title insurance ordered and tracked online.

- Digital escrow setup for earnest money deposits and closing funds.

- Secure portals for document collection and status updates.

- Remote Online Notarization (RON) or hybrid e‑signing for eligible documents.

- Electronic recording of deeds and mortgages where the county accepts eRecording (Albany County does).

In New York, attorneys are typically involved for both sides. The title company, lender, and attorneys coordinate through shared portals or secure email. Even in a “digital” closing, some documents may still need wet ink, depending on lender policy and the exact document type.

What’s different about using them to buy in Albany and the Capital Region?

- Attorney-driven closings: Most buyers retain a New York attorney. Online tools coordinate work but do not replace legal review.

- Mortgage recording tax: Albany County collects mortgage recording tax. Calculations and filings must be correct to avoid rejections or delays.

- Survey and municipal nuances: In the Capital Region, questions about boundary lines, private roads, wells, septics, and certificates of occupancy can surface late. Digital workflows help track tasks, but resolution may require local inspections and municipal visits.

- County eRecording: Albany County supports eRecording, which speeds up post‑closing. Neighboring counties vary in processing times, which affects when you get the recorded deed.

Typical steps of the process when buying a home using digital services

1) Right after the contract is signed

- Open title: Your attorney or the title provider orders the title search.

- Open escrow: A digital escrow is created for earnest money and future funds.

- Lender loan file: You authorize document sharing through the secure portal.

2) Title search and underwriting

- Public records: Liens, judgments, easements, and prior deeds are reviewed.

- Survey matters: A new or updated survey may be ordered, which can be a bottleneck if the property has boundary or fence questions.

- Commitment issued: The title commitment lists requirements to clear before closing (e.g., payoff amounts, municipal certificates, HOA letters).

3) Escrow deposits and wiring

- Earnest money: Sent by wire or electronic transfer to the escrow holder. A verified call before wiring reduces fraud risk.

- Closing funds: Final numbers arrive from the lender and attorney via Closing Disclosure and settlement statement. You then wire funds securely.

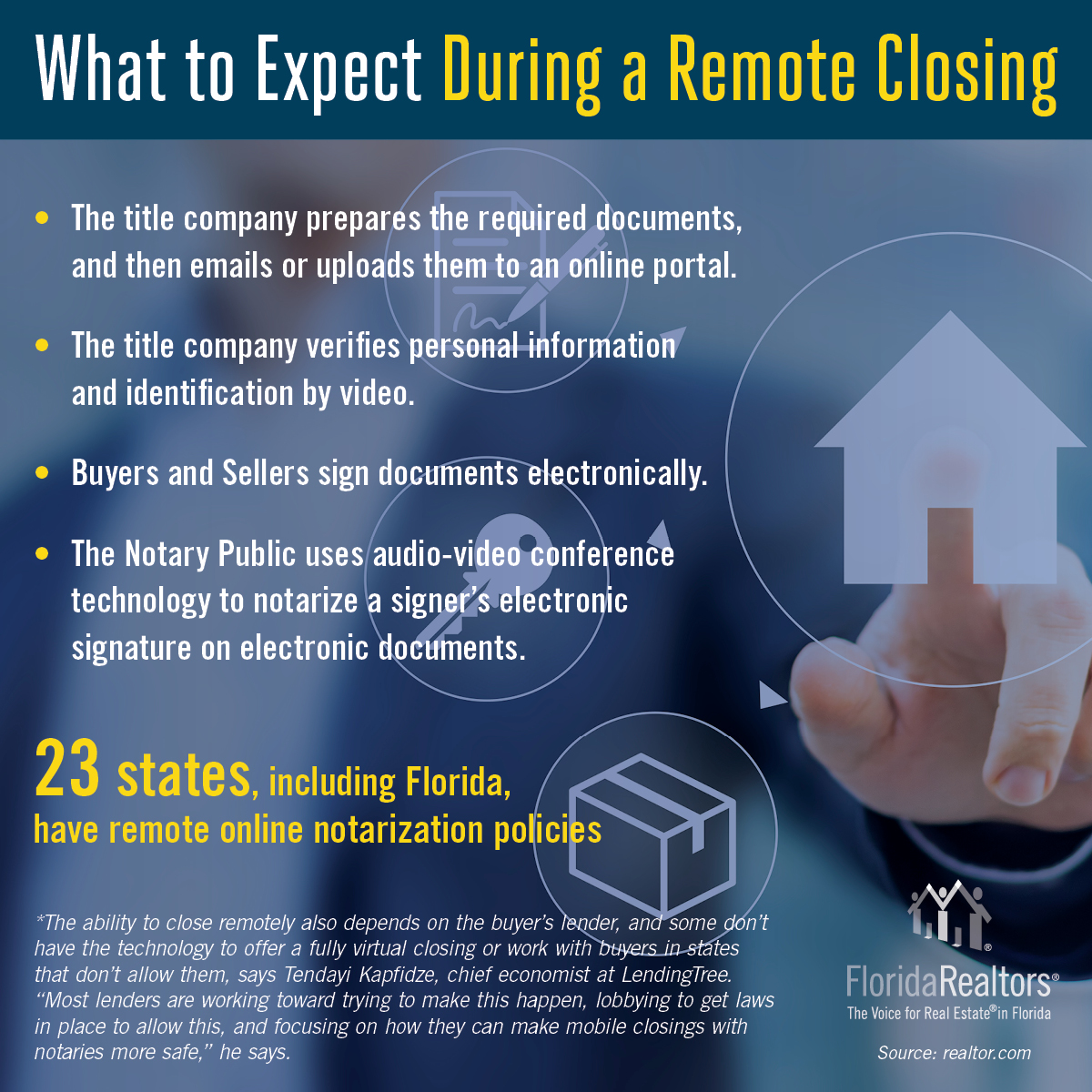

4) Signing and notarization

- Hybrid or RON: Many buyers e‑sign non‑notarized forms, then use an approved New York RON notary for notarized documents. Some lenders still require wet signatures on the note or mortgage.

- ID checks: Expect knowledge‑based authentication and credential analysis during RON.

5) Funding and recording

- Funding: Lender wires proceeds into escrow once all conditions are met.

- eRecording: Deed and mortgage are submitted to the county. Confirmation can arrive within hours or a few days, depending on county workflow.

Costs, savings, and potential tradeoffs

Expect the usual New York buyer costs plus a few digital line items. Here’s a simplified view:

| Item | Typical Range in Albany Area | Notes |

|---|---|---|

| Title insurance (owner & lender) | Regulated rates | Rates set by NY rules; vary by purchase price and loan. |

| Title search/endorsements | $300–$900+ | Property specifics drive endorsements. |

| Attorney fee | $900–$2,000+ | Complexity and firm practice vary. |

| Escrow/settlement fee | $400–$1,000 | Depends on provider and scope. |

| RON/e‑notary fee | $25–$150 per session | Sometimes bundled. |

| Courier vs. e‑delivery | $0–$100 saved | Digital flow reduces overnighting. |

| Mortgage recording tax | Varies by loan amount | Albany County applies state and local portions. |

Tradeoffs:

- Fewer trips and faster document exchange vs. the occasional need to pivot to wet signatures.

- Lower courier and scheduling friction vs. time spent on ID verification and portal logins.

- Quicker post‑closing eRecording vs. the same title insurance costs (since those are regulated).

Risks and protections when closing online

- Wire fraud: The largest risk. Use call‑back protocols to a known office number before sending funds. Do not trust emailed wiring changes.

- Identity theft: RON platforms use multi‑factor checks and credential analysis. If anything feels off, pause and confirm through your attorney.

- Document errors: Digital speed can hide mistakes. Ask for a full pre‑close package review with your attorney and lender.

- Data privacy: Confirm your title/escrow provider’s security practices. New York’s privacy standards apply; vendors should align with them.

- Recording rejection: Even with eRecording, county clerks can reject documents for small errors. Local experience helps avoid rework.

Timeline comparison: standard closing vs online‑assisted

| Milestone | Standard (Albany) | Online‑assisted | What changes |

|---|---|---|---|

| Earnest money delivered | 1–3 days (mail/courier) | Same day or next day (wire) | Digital escrow speeds funding. |

| Title search & commitment | 10–14 business days | 7–12 business days | Faster ordering and tracking. |

| Survey ordered/reviewed | 1–3 weeks | 1–3 weeks | No major digital gains; vendor timing rules. |

| Document review/signing | In‑office scheduling | RON/hybrid in 1–2 sessions | Flexible timing, fewer trips. |

| Recording confirmation | 2–7 days after close | Hours to a few days | eRecording reduces lag. |

Overall, we see 3–7 days saved in clean files. Issues like boundary disputes or appraisal delays erase those gains regardless of digital tools.

Local buyer concerns: remote service, local oversight, trust factors

- Remote vs. local: Using a national online platform is convenient, but Albany and surrounding counties have quirks. A local attorney and locally active title team reduce surprises.

- Trust: Ask how funds are held, how wires are verified, and what insurer backs the title policy.

- Transparency: Request a clear portal timeline and named contacts for underwriting, escrow, and recording.

If you’re coordinating a sale and a purchase, online workflows can help you close both on the same day. For sellers looking to sell their house fast in albany new york, the same secure wiring and eRecording tools can shorten the gap between sales proceeds and purchase funds. The key is early scheduling across both files.

How these services affect coordination with agents, lenders, and attorneys

- Agents: Shared checklists and status portals reduce back‑and‑forth. Property access for inspections remains arranged locally.

- Lenders: Some lenders are fully e‑close capable, others allow hybrids, and a few still require in‑person signing for certain documents. Confirm at loan application.

- Attorneys: In New York, attorneys are central. They review the contract, title, and closing package, whether you sign online or in person.

For a broader understanding of the closing sequence in this region, see this expert closing guide for Upstate NY buyers. It pairs well with online workflows because you can anticipate when an e‑step is allowed and when a wet signature or local visit may still be required.

When online title/escrow may not work well in Upstate NY

- Complex survey issues: Encroachments, shared driveways, or private road maintenance agreements often require in‑person resolution with neighbors or municipalities.

- Properties with wells and septics: Testing, permits, and repairs are hands‑on and can affect title conditions.

- Condo/HOA approvals: Some boards require original signatures or physical packages.

- Specific lender restrictions: A few loan programs or institutions still prohibit RON for certain documents.

- Short‑notice closings: Oddly, rushing can push you back to paper if a RON notary or platform approval isn’t available on the needed day.

Case scenarios: first‑time buyer, remote buyer, tight deadline

First‑time buyer in Albany

Scenario: You rent in the city and buy a starter home in the Helderberg neighborhood. You work standard office hours.

What helps: A portal to upload pay stubs and insurance info, wire earnest money, and e‑sign non‑notarized disclosures after work. One short RON session handles notarized forms. You still coordinate with your attorney on the title commitment, survey letter, and final walk‑through scheduling.

Extra reading for planning grants and programs: first-time buyer assistance in 2025.

Remote buyer relocating to the Capital Region

Scenario: You live in another state and want to close without flying in.

What helps: RON authorization, online escrow, and eRecording. If your lender requires a wet-signed note, your attorney may arrange a mobile notary or a limited in‑person session where you are. Confirm state‑to‑state notary acceptability and shipping buffers if any wet ink is involved.

Tight deadline buyer aligning a sale and a purchase

Scenario: You’re selling a home in Colonie and buying in Albany on the same day.

What helps: Early verification of both lenders’ closing styles, clear wire timing for proceeds, and eRecording to confirm transfer fast. If you’re also thinking about optimizing your sale path and looking to sell your house fast in albany new york, digital escrow and verified wiring reduce idle time between the two closings.

Checklist: how to prepare if you’re planning to use online services

- Ask your lender upfront: full e‑close, hybrid, or paper only?

- Choose a title/escrow provider that supports RON and Albany County eRecording.

- Confirm your attorney’s comfort with digital platforms and portal sharing.

- Set wire safety rules: no changes accepted by email, call back on a known number.

- Gather IDs that pass RON checks (unexpired, scannable photo ID).

- Schedule survey orders early if any boundary, fence, or acreage questions exist.

- Verify HOA or municipal approvals and payoff letters well before closing.

- Test your tech: stable internet, camera, and a quiet space for the RON session.

- Review the full package 24 hours before signing; list questions for your attorney.

- Confirm recording ETA and how you will receive the recorded deed and final policy.

FAQ from buyers considering these tools for the first time

Can I close completely online in Albany?

Sometimes. Many files are hybrid: e‑sign what you can, notarize remotely, and record electronically. A few lenders still require wet signatures on certain documents.

Is Remote Online Notarization legal in New York?

Yes, subject to platform and identification standards. Not every lender accepts RON for every document. Your attorney will align the plan with lender policy.

How do I avoid wire fraud?

Call your escrow holder at a verified number to confirm wiring details before you send funds. Do not act on wiring changes received by email or text.

Do online tools speed up appraisals, inspections, or surveys?

No. Those depend on local vendor calendars. Digital scheduling helps, but availability drives timing.

What if I’m searching for options “near me” but buying in Albany?

“Near me” reflects intent. For an Albany purchase, pick providers who routinely close in the Capital Region. Local familiarity matters more than proximity to your current address.

Will online escrow change my closing costs?

Title insurance rates are regulated. Expect minor savings on courier and coordination time, plus possible RON fees. The net is usually modest but meaningful.

Can the same tools help if I need to sell before I buy?

Yes. Coordinated digital workflows help align proceeds and purchase funds. Sellers who ask about “how to sell my house fast in albany new york” are often focused on timeline control; online escrow, verified wires, and eRecording help manage same‑day or back‑to‑back closings.

Conclusion

Online title and escrow services are most useful in Albany when they complement, not replace, the attorney‑led structure of a New York closing. They cut friction on routine steps and support tighter timelines, especially for remote buyers and coordinated same‑day deals. Their limits show up around surveys, lender exceptions, and municipal quirks. If you treat digital tools as a framework and keep local professionals at the center, you gain speed without losing control over details that decide whether your closing is smooth or stressful.